Marketers Most Wanted: August 2025

After a turbulent few months of movement within the top three, August’s Marketers Most Wanted sees Software Development return to the number one position. The shift signals a renewed focus on digital infrastructure, platform improvement and technical delivery, as brands start building momentum for H2.

We’re also seeing the re-emergence of some core categories - including CRM, which makes its first appearance in the top ten - as well as interesting developments in content, creative, and integrated campaign briefs.

StudioSpace is an agency/client matchmaking platform, monitoring real-time briefs we receive from chief marketing officers (CMOs) and brand owners. This information gives us a unique perspective on what’s hot and what’s not each month - data which is then distilled into our monthly Marketer’s Most Wanted report.

Software Development is back on top

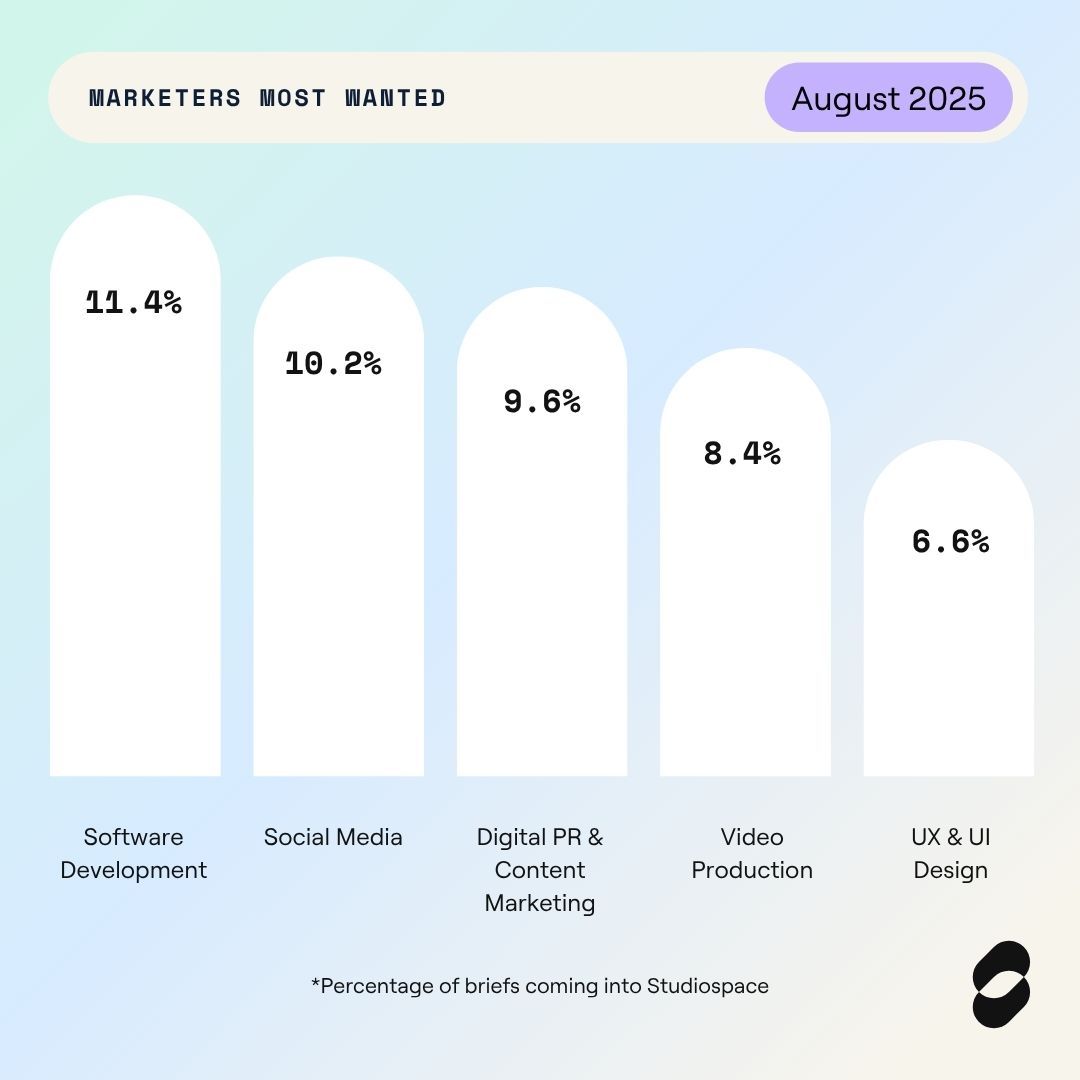

After falling from first place in May to fourth by June, Software Development has steadily climbed its way back to the top. It now leads the table with 11.4% of briefs - its highest share this year. This category continues to reflect the business-critical role of technology, especially as many brands shift focus from strategy and design to implementation and build.

We’ve seen a real breadth of activity this month, from scalable platform development to highly targeted web optimisation and systems integration. The uptick may also reflect a push from marketing and digital teams to prepare for autumn launches or end-of-year performance goals.

Our CEO Pete Sayburn comments:

We’re seeing a real appetite from brands to make technical progress - from new app and web builds to addressing long-standing development backlogs. It’s no surprise to see Software Development topping the table again, especially as we move out of the summer period and into the final push of the year."

Social Media still strong, despite a slight dip

This month, Social Media drops to second place (10.2%, down from 10.8%) but continues to attract consistent demand from brands across sectors. Both organic and paid briefs are flowing through the platform, with TikTok and LinkedIn remaining the dominant platforms of choice - suggesting a slight tilt away from Meta as the year progresses.

Although the percentage share has dipped slightly, the category is still central to how brands engage and grow communities. We’re seeing an increase in requests for social strategy refreshes, platform-specific content, and influencer-led campaigns.

A strong month for content

Digital PR & Content Marketing climbs back into the top three this month, increasing its share by 1.2%. The projects in this category range from evergreen content and editorial development through to reactive digital PR and long-form storytelling. We’re also seeing increased demand for copywriting, brand tone of voice work, and multi-format content designed to engage specific audiences.

The consistent growth in this category reinforces the idea that creativity and quality continue to cut through - especially in saturated markets or during peak periods of digital activity.

“It’s encouraging to see brands recognising the value of strong content again,” says Pete. “There’s a real focus right now on targeted, relevant materials that serve specific user journeys - whether that’s in B2C, B2B or internal campaigns.”

Video dips again - but budgets rise

Video Production drops one place this month, falling to fourth with a share of 8.4%. This marks a continued decline since it topped the table in June - but interestingly, this category represents the highest average project value on the platform this month.

While volume may be down, investment is clearly up - with several briefs involving large-scale shoots, high-end production, and complex post-production requirements. Brands appear to be commissioning fewer videos overall, but placing more value on quality and creative ambition when they do.

UX, Insight and Product - a mixed middle

In the middle of the table, we’re seeing some familiar movement:

- UX & UI Design drops again to fifth, down 1.8% this month. The category has been more volatile in 2025 than it was last year, where it consistently sat in the top half of the table. Current briefs range from microsite redesigns and feature-specific UX optimisation to fully embedded UX teams within brand-side squads.

- Research & Insight holds steady at 6.6% but gains one place in the rankings. Projects this month span persona development, sentiment analysis, brand perception studies and competitor benchmarking - with briefs often coming from marketing leads looking to de-risk decisions heading into H2.

- Product & Proposition sees a drop in share this month (down from 6.6% to 5.4%), moving to 7th place. There’s still active demand, particularly from the Australian market, with briefs focused on go-to-market strategy, new product development and value proposition design.

CRM enters the top 10

Making its debut in the top ten this month is CRM, now at 9th place with 4.8% of briefs. This is the first time this category has appeared in the rankings - but it’s been bubbling just below the surface in previous months.

We’re seeing a real mix of activity: from strategic audits and CRM architecture through to copy and campaign development within specific platforms like HubSpot, Salesforce, and Klaviyo. This rise suggests brands are paying more attention to customer lifecycle management, loyalty and retention.

“CRM is where brands are really starting to look for sustainable growth,” says Sayburn. “It’s no longer just about acquisition - there’s a real shift toward improving comms, data use and automation across the customer journey.”

Integrated Campaigns and Paid Media stay stable

- Digital Marketing Campaigns (Integrated) stays flat this month in terms of share and position. Brands appear to be investing in campaign amplification rather than starting fresh initiatives - a seasonal trend that often aligns with summer holidays and stakeholder availability.

- Digital Paid Media remains in 10th place for the fourth consecutive month, with a slight drop of 0.6%. With performance marketing often tied to spend windows and product launches, we’ll be watching to see if this category rebounds in September and October.

Dropping out

After a brief appearance in July’s top 10, Creative Campaign has dropped out this month. While we’ve seen some high-quality briefs in this space recently, it’s possible that brands are holding back on larger creative projects until Q4 - or exploring them within wider integrated campaigns instead.

As we head into the final stretch of summer, it’s clear that brands are laying the groundwork for a strong finish to 2025. With Software Development back in the top spot and CRM making its first appearance in the top ten, there’s a noticeable shift toward delivery, infrastructure, and owned customer journeys.

Conclusion

While creative categories like Video and Content remain strong, and Social Media continues to be a mainstay, the quiet rise of more technical and strategic categories suggests that brands are preparing for long-term growth - not just short-term campaigns.

We’ll be keeping a close eye on how these trends evolve as we move into Q4 planning season, and whether we see a seasonal surge in creative and integrated campaign work once the summer slow-down begins to lift.

As always, we’ll be back next month with the latest category movements and insight into what brands are buying right now.

To view last month’s report, click here